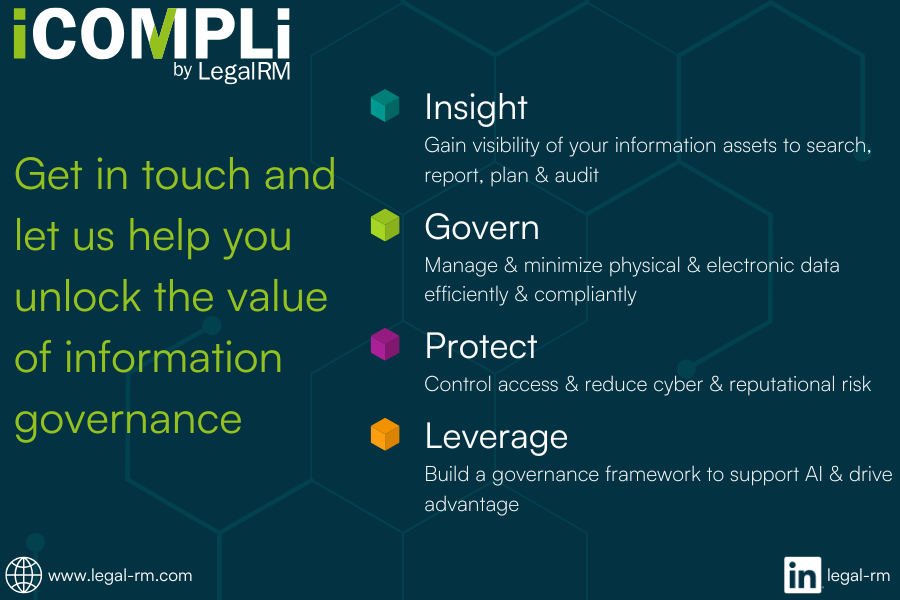

Accountancy practice management software has come a long way. Today, features like automated billing and reconciliations are easily integrated into the day-to-day practice workflow of Wolters Kluwer Tax & Accounting UK customers.

Our employees work side by side with our customers to create and manage these solutions – driven by a deep understanding of their needs and addressing the rapid changes in their environment.

However, it’s often hard to look beyond improving performance in day-to-day operations. Amid Brexit, the COVID-19 pandemic and other disruptions, accountancy practices and their clients are dealing with an unpredictable economic landscape. Future business planning can appear daunting.

However, technology can support accountancy practices (and their clients) in making informed business decisions, and planning for the future. In the first part of our Accountancy Practice Management for Future-Fit Growth series, we’ll explore how they can use technology to define and easily track Key Performance Indicators (KPIs). Doing so gives practices closer control of performance tracking, and deeper insights that will inform strategic growth plans.

Saving Time

For several decades, business technology platforms have enabled practices to track performance metrics that they have customised. This highlights areas that qualify for improvement and underpins strategic planning.

Contemporary technology, such as CCH KPI Monitoring, makes setting up KPIs faster and easier for accountancy practices than ever before. This is vital today. The current business landscape demands that firms assess and amend KPIs more frequently, based on fresh market variables. KPIs such as client retention rate and business time-to-recovery have become increasingly prominent performance indicators in the past year. If clunky technology makes KPI management difficult, practices have less time and insight to plan future growth.

.jpg)

Reducing Risk

CCH KPI Monitoring makes it far easier to track KPIs and report on them. This is fundamental in minimising risk. For example, if a KPI is set to track and escalate debt filtered by overdue dates, the ability to easily set alerts and automatically generate reports is critical to practice performance management.

Some practices are manually running monthly reports to measure KPIs. Others are running real-time reporting engines, a key feature of CCH KPI Monitoring. This latter solution allows practices to review essential data at any time – covering both performance management and compliance requirements. They can do so remotely or on-premise.

This means that firms can assess issues before they become problems, and thus act proactively. Real-time reporting is a true asset in building a future-fit practice.

The Proof is in the Practice

A number of Wolters Kluwer customers have been using CCH KPI Monitoring for several years now. Our customers look to us when they need to be right. Ryecroft Glenton has successfully integrated CCH KPI Monitoring with its own system. This consolidates information from several sources, including CCH Central and CCH Practice Management.

“We can use the year end date to trigger a sequence of reminders. Have we asked for the books? Have they been received? If a request to a client has been outstanding for a certain period, the partner will receive an alert via email. For limited companies, we can monitor the corporation tax and Companies House filing deadlines – as well as the different deadlines for pension schemes”

– Ian Smith, partner at Ryecroft Glenton

.jpg)

Corporate events agency who benefited from greener graphics initiative

“Apogee are not just aprinting company, theyconsult with us and go onto deliver a full end to endservice from concept toinstallation. They go aboveand beyond and we lookforward to continuing ourjourney with them”

Corporate events agency who benefited from greener graphics initiative

“Apogee are not just aprinting company, theyconsult with us and go onto deliver a full end to endservice from concept toinstallation. They go aboveand beyond and we lookforward to continuing ourjourney with them”

Corporate events agency who benefited from greener graphics initiative

“Apogee are not just aprinting company, theyconsult with us and go onto deliver a full end to endservice from concept toinstallation. They go aboveand beyond and we lookforward to continuing ourjourney with them”

Corporate events agency who benefited from greener graphics initiative

“Apogee are not just aprinting company, theyconsult with us and go onto deliver a full end to endservice from concept toinstallation. They go aboveand beyond and we lookforward to continuing ourjourney with them”

.jpeg)

.png)